Last month, I wrote about mold under your flooring.

Water damage in your home can feel overwhelming and stressful. A leak can soak your floor in minutes. Then you sit wondering if your homeowners' insurance will help, how to start an insurance claim, and what repairs you should do first.

This is general information. Your coverage depends on your policy and your insurance company.

What To Do After Water Damage and a Leak

The first step when water damage occurs is to take action fast. Quick steps can help prevent bigger problems.

- Stop the leak if you can. Shut off the valve or water source.

- If it is safe, turn off the power near wet areas.

- Move water away from the damaged area. Use towels, a wet vac, or a mop.

- Start the cleanup and drying. Use fans and a dehumidifier if you have one.

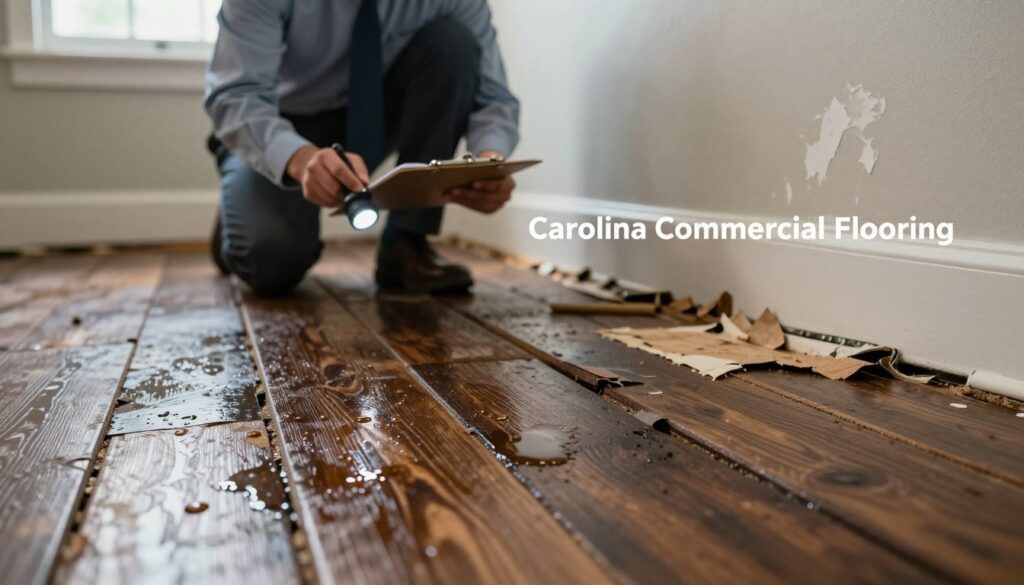

- Take photos from multiple angles. Wide shots and close-ups both help.

- Keep a simple note of what happened and when the water event started.

If there is standing water or you smell mold, call a restoration team or a damage restoration company for help.

Insurance Coverage and Water Damage Coverage

If you have homeowner’s insurance, you might be in luck. I said might. Many homeowners' insurance plans (also called home insurance) may cover sudden and accidental water damage. This is water damage that occurs quickly and is unplanned.

Examples that may be covered by your insurance:

- A burst pipe

- A water heater that breaks

- A washing machine hose that suddenly fails

- An appliance overflow that happens fast

But some damage isn’t covered. Many insurance policies have an exclusion for:

- A slow leak

- Ongoing seepage

- Wear and tear or normal wear and tear

- Damage from poor home maintenance

Always check your policy details. Understanding your policy helps you avoid surprises.

Flood Damage and Separate Flood Insurance

Flooding is often treated differently from a burst pipe. Many times, a standard homeowners' policy does not cover floodwater that comes from outside.

If you live in a flood-prone area, you may need flood insurance. Many people get it through the National Flood Insurance Program. In many cases, it is separate flood insurance from your standard homeowners coverage.

If water seeps in from the ground, or you have damage from heavy rain and outside flooding, ask your insurance agent what applies.

Signs of Water Damage in Your Floor and Damaged Area

Some signs show up right away. Others hide under the surface.

Signs of water damage you can see:

- Bubbling or peeling

- Dark stains or discoloration

- Soft spots or spongy areas

- Warping, cupping, or buckling

Floor type matters:

- Hardwood floors can warp and buckle.

- Laminate flooring can swell and lift.

- Tile may look fine on top, but the subfloor may be wet.

If the damaged area smells musty, the layer under the floor may be wet. That can lead to bigger water damage repairs later.

Water Damage Insurance Claims: How to Start an Insurance Claim and Contact Your Insurance Company

To start a water damage claim, you usually need to report it fast. Many policies require quick notice.

Steps for the claims process:

- Contact your insurance company and ask how to report the damage.

- Ask what documents they need for the insurance claim.

- Share your photos (remember: multiple angles).

- Write a short list of what got damaged (floors, baseboards, cabinets).

- Save every receipt for emergency supplies or services.

- Get repair estimates from pros, if your insurer asks.

Ask your insurer what to do before you remove too much material. Some insurance companies want to see the damage first.

Adjuster Visit and Insurance Company Payout: Replacement Cost, Actual Cash Value, Out-of-Pocket Costs

After you file, the insurance company may send an adjuster. The adjuster checks the damage and compares it to your homeowners' policy.

Your payout can depend on your coverage type:

- Replacement cost: may pay to replace items with similar new items (minus your deductible).

- Actual cash value: may pay less because it includes age and use.

You may also have out-of-pocket costs:

- Your deductible (what you pay first)

- Costs above limits, if your policy has caps per claim

Ask your insurer how your plan handles flooring. Some plans treat floors differently from furniture.

Claim Denials and Damage Claim Appeals

Sometimes, people face claim denials. This can happen for reasons like:

- The damage is linked to a long-term leak (not sudden)

- The insurer says the issue is wear and tear

- Missing photos, notes, or receipts

- The report was late, and policies require quicker notice

If you get a denial:

- Ask for the reason in writing.

- Review your policy details and the exclusion used.

- Send more proof (photos, repair estimates, timelines).

- Ask how to appeal the decision.

Some homeowners choose to hire a public adjuster for a hard damage claim. That choice depends on your situation.

Repair or Replace: Whole Floor vs Spot Fix, Water-Damaged Floors, Water Damage Repairs

After water damage, the big question is often: repair or replace?

A small spot may be repairable if:

- The subfloor is dry and solid

- Only a small damaged area is affected

- The flooring product still matches

But full replacement may make sense if:

- The floor is buckled, swollen, or soft

- Water got under the floor

- The subfloor is damaged

- Matching the floor is not possible

Sometimes replacing the whole floor gives the best look and helps restore your home back to its original feel.